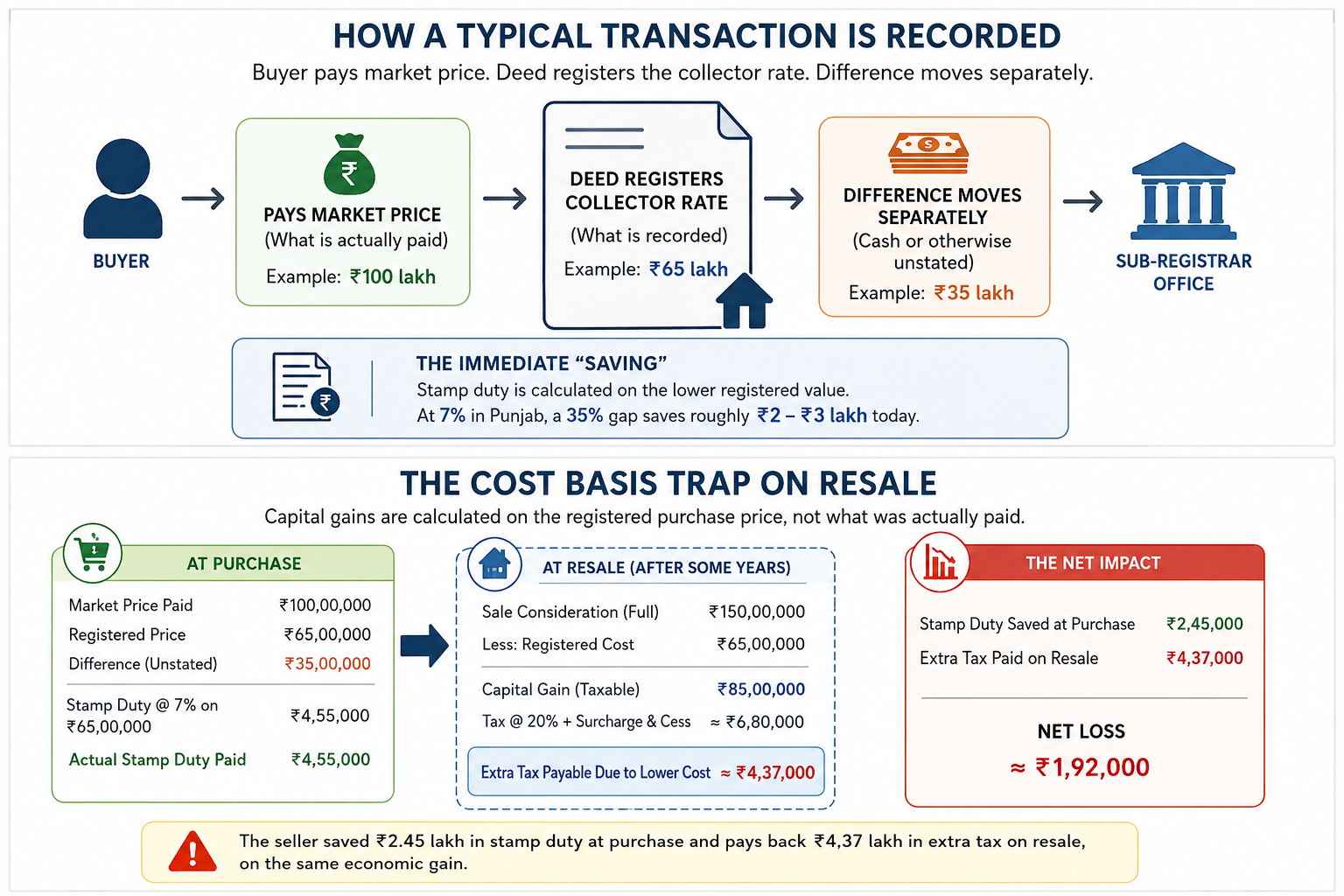

In a typical Mohali property transaction, the price on the brochure and the price on the registry deed are not the same number. The first is what gets paid; the second is what gets recorded, usually 30 to 50 per cent lower, with the gap moving in cash or otherwise unstated.

At a glance

Punjab's collector rate is a floor for stamp duty, not a record of market price

The October 2025 Mohali revision raised residential rates 20 to 22 per cent, and the gap remains

Section 50C locks the seller's deemed sale value at the collector rate

Section 56(2)(x) taxes the buyer when registered value is more than 10 per cent below SDV

The bigger trap is the cost basis lock-in that bites on resale

Why the gap exists

The collector rate, also called the circle rate, is the minimum value below which a property cannot be legally registered. It governs stamp duty calculation, not actual market price, and is revised annually by the district administration. Mohali's most recent revision came into force on 23 October 2025, with residential rates up 20 to 22 per cent and industrial up 30 per cent.A buyer pays the market price while the deed registers the collector rate. The visible "saving" is the stamp duty calculated on the lower number, which at Punjab's 7 per cent rate works out to roughly ₹2 to 3 lakh on a 35 per cent gap. That is the figure shown to the buyer at registration; the real cost shows up years later.

The cost basis trap on resale

When the buyer eventually sells, the cost of acquisition for capital gains is the registered purchase price, not what was actually paid. The Income Tax Act tracks paperwork, and cash receipts do not count toward cost. This means the capital gain on resale is computed from the lower registered cost, producing a phantom gain the seller pays tax on even though the real economic gain is much smaller.

The seller saved ₹2.45 lakh in stamp duty at purchase and pays back ₹4.37 lakh in extra tax on resale, on the same economic gain. The break-even has flipped against the seller, and the cash component still needs to be legitimized somehow before it can be used, banked, or repatriated.

Section 50C and Section 56(2)(x)

Section 50C of the Income Tax Act locks this trap further on the seller side. If the seller tries to under-register the sale to keep the recorded gain small, Section 50C treats the higher of the actual sale price or the current collector rate as the deemed sale consideration. The seller cannot escape the gain even by repeating the same understatement on exit.

Section 56(2)(x) is the buyer's mirror. If the buyer's recorded consideration is more than 10 per cent below the stamp duty value, the difference is taxed as income from other sources in the buyer's hands. In Mohali this rarely fires because buyers register at exactly the collector rate, but the exposure becomes live when collector rates move sharply, as in October 2025.

The NRI angle

For NRI sellers, the trap compounds. TDS under Section 195 is deducted at 20 per cent of the entire sale consideration for long-term capital assets, plus surcharge and cess, not just on the gain. A lower registered cost means a higher computed gain, a smaller refund, and a slower repatriation, because banks will not remit the cash portion without a CA-certified Form 15CB showing source of funds.

The practical path

Registering at actual transaction value carries a higher stamp duty bill today, but eliminates the trap entirely and usually breaks even within the first holding period. For buyers using bank finance the question rarely arises in practice, because lenders will only disburse against the registered value, not against any side cash arrangement.

₹2-3 lakh more in stamp duty today

₹4-5 lakh less in capital gains tax on resale

Clean repatriation for NRIs through normal banking channels

No cash component to handle, store, or explain later

No Section 148 scrutiny risk at the back end

Bottom line

The Mohali registry value is not the market price. The collector rate is a floor for stamp duty, not a record of what changed hands, and whatever is saved at registration is usually paid back on resale with a layer of cash and audit risk on top. SourcesIncome Tax Act, 1961. Section 50C, Section 56(2)(x), Section 195. Government of India.

Punjab Stamp Act and Indian Registration Act, 1908.

District Administration, SAS Nagar (Mohali). Notification of revised collector rates effective 23 October 2025.

The Tribune. "Mohali implements new collector rates." 24 October 2025.

CityNest Realty. "Mohali Property Prices to Increase as Collector Rates Rise from October 23." 15 October 2025.

Garah Pravesh. "Collector Rates Hiked up to 67% in Mohali." November 2025.

ClearTax. "Section 50C of Income Tax Act: Taxability of Sale of Land or Building."

This article is general information as of May 2026, not tax or legal advice. mohaliaerotropolis.com is not a tax adviser. Buyers, sellers, and NRIs should consult a qualified chartered accountant for any specific transaction.

शीर्षक (संदर्भ के लिए): आपका मोहाली रजिस्ट्री मूल्य लेन-देन की कीमत से 30 से 50 प्रतिशत कम क्यों है: पुनर्विक्रय पर कलेक्टर दरें और पूंजीगत लाभ का जाल

एक सामान्य मोहाली संपत्ति लेन-देन में, ब्रोशर पर कीमत और रजिस्ट्री डीड पर कीमत एक ही संख्या नहीं होती है। पहली वह है जो वास्तव में भुगतान की जाती है; दूसरी वह है जो दर्ज की जाती है, आमतौर पर 30 से 50 प्रतिशत कम, और यह अंतर नकद या अन्य अनिर्दिष्ट तरीकों से चलता है।

एक नज़र में

- पंजाब की कलेक्टर दर स्टांप शुल्क के लिए एक न्यूनतम सीमा है, बाजार मूल्य का रिकॉर्ड नहीं

- अक्टूबर 2025 के मोहाली संशोधन ने आवासीय दरों में 20 से 22 प्रतिशत की वृद्धि की, और अंतर बना हुआ है

- धारा 50C विक्रेता के कथित विक्रय मूल्य को कलेक्टर दर पर सीमित कर देती है

- धारा 56(2)(x) खरीदार पर तब कर लगाती है जब पंजीकृत मूल्य SDV से 10 प्रतिशत से अधिक कम हो

- बड़ा जाल लागत आधार का लॉक-इन है जो पुनर्विक्रय पर नुकसान पहुंचाता है

अंतर क्यों मौजूद है

कलेक्टर दर, जिसे सर्कल रेट भी कहा जाता है, वह न्यूनतम मूल्य है जिससे नीचे किसी संपत्ति को कानूनी रूप से पंजीकृत नहीं किया जा सकता। यह स्टांप शुल्क गणना को नियंत्रित करती है, वास्तविक बाजार मूल्य को नहीं, और जिला प्रशासन द्वारा प्रतिवर्ष संशोधित की जाती है। मोहाली का सबसे हालिया संशोधन 23 अक्टूबर 2025 को लागू हुआ, जिसमें आवासीय दरों में 20 से 22 प्रतिशत और औद्योगिक दरों में 30 प्रतिशत की वृद्धि हुई।

एक खरीदार बाजार मूल्य का भुगतान करता है जबकि डीड कलेक्टर दर दर्ज करती है। दिखने वाली "बचत" स्टांप शुल्क है जो कम संख्या पर गणना की जाती है, जो पंजाब की 7 प्रतिशत दर पर 35 प्रतिशत के अंतर पर लगभग ₹2 से 3 लाख होती है। पंजीकरण के समय खरीदार को यही आंकड़ा दिखाया जाता है; वास्तविक लागत वर्षों बाद सामने आती है।

पुनर्विक्रय पर लागत आधार का जाल

जब खरीदार अंततः बेचता है, तो पूंजीगत लाभ के लिए अधिग्रहण की लागत पंजीकृत खरीद मूल्य होती है, न कि वास्तव में भुगतान की गई राशि। आयकर अधिनियम कागजी कार्रवाई को ट्रैक करता है, और नकद प्राप्तियां लागत में नहीं गिनी जाती हैं। इसका मतलब है कि पुनर्विक्रय पर पूंजीगत लाभ की गणना कम पंजीकृत लागत से की जाती है, जिससे एक काल्पनिक लाभ उत्पन्न होता है जिस पर विक्रेता कर चुकाता है, भले ही वास्तविक आर्थिक लाभ बहुत छोटा हो।

विक्रेता ने खरीद पर स्टांप शुल्क में ₹2.45 लाख बचाए और पुनर्विक्रय पर अतिरिक्त कर में ₹4.37 लाख चुकाता है, उसी आर्थिक लाभ पर। स्थिति विक्रेता के विरुद्ध हो गई है, और नकद घटक को अभी भी किसी तरह वैध बनाने की आवश्यकता है, इससे पहले कि इसका उपयोग, बैंकिंग या प्रत्यावर्तन किया जा सके।

धारा 50C और धारा 56(2)(x)

आयकर अधिनियम की धारा 50C विक्रेता की ओर से इस जाल को और मजबूत करती है। यदि विक्रेता दर्ज लाभ को छोटा रखने के लिए बिक्री को कम पंजीकृत करने का प्रयास करता है, तो धारा 50C वास्तविक विक्रय मूल्य या वर्तमान कलेक्टर दर में से जो अधिक हो, उसे कथित विक्रय प्रतिफल मानती है। विक्रेता बाहर निकलने पर भी वही कम बताना दोहराकर लाभ से बच नहीं सकता।

धारा 56(2)(x) खरीदार का दर्पण है। यदि खरीदार का दर्ज प्रतिफल स्टांप शुल्क मूल्य से 10 प्रतिशत से अधिक कम है, तो अंतर को खरीदार के हाथों में अन्य स्रोतों से आय के रूप में कर योग्य माना जाता है। मोहाली में यह शायद ही कभी लागू होता है क्योंकि खरीदार ठीक कलेक्टर दर पर पंजीकरण कराते हैं, लेकिन जोखिम तब सक्रिय हो जाता है जब कलेक्टर दरों में तेजी से बदलाव होता है, जैसा कि अक्टूबर 2025 में हुआ।

NRI कोण

NRI विक्रेताओं के लिए, यह जाल और बढ़ जाता है। धारा 195 के तहत TDS दीर्घकालिक पूंजीगत संपत्तियों के लिए पूरे विक्रय प्रतिफल के 20 प्रतिशत पर काटा जाता है, साथ ही अधिभार और उपकर, न कि केवल लाभ पर। कम पंजीकृत लागत का मतलब उच्च गणना लाभ, छोटा रिफंड और धीमा प्रत्यावर्तन है, क्योंकि बैंक धन के स्रोत को दर्शाने वाले CA-प्रमाणित फॉर्म 15CB के बिना नकद हिस्से को रेमिट नहीं करेंगे।

व्यावहारिक रास्ता

वास्तविक लेन-देन मूल्य पर पंजीकरण करने पर आज अधिक स्टांप शुल्क का बिल आता है, लेकिन यह जाल को पूरी तरह से समाप्त कर देता है और आमतौर पर पहली होल्डिंग अवधि के भीतर ही बराबर हो जाता है। बैंक वित्तपोषण का उपयोग करने वाले खरीदारों के लिए, यह सवाल व्यवहार में शायद ही कभी उठता है, क्योंकि ऋणदाता केवल पंजीकृत मूल्य के विरुद्ध धन जारी करेंगे, किसी भी साइड कैश व्यवस्था के विरुद्ध नहीं।

- आज स्टांप शुल्क में ₹2-3 लाख अधिक

- पुनर्विक्रय पर पूंजीगत लाभ कर में ₹4-5 लाख कम

- NRIs के लिए सामान्य बैंकिंग चैनलों के माध्यम से स्वच्छ प्रत्यावर्तन

- बाद में संभालने, संग्रहीत करने या समझाने के लिए कोई नकद घटक नहीं

- पीछे के छोर पर कोई धारा 148 जांच जोखिम नहीं

निचली पंक्ति

मोहाली रजिस्ट्री मूल्य बाजार मूल्य नहीं है। कलेक्टर दर स्टांप शुल्क के लिए एक न्यूनतम सीमा है, न कि इस बात का रिकॉर्ड कि वास्तव में क्या हस्तांतरित हुआ, और पंजीकरण पर जो बचाया जाता है, वह आमतौर पर नकद और ऑडिट जोखिम की एक परत के साथ पुनर्विक्रय पर चुकाया जाता है।

स्रोत

- आयकर अधिनियम, 1961। धारा 50C, धारा 56(2)(x), धारा 195। भारत सरकार।

- पंजाब स्टांप अधिनियम और भारतीय पंजीकरण अधिनियम, 1908।

- जिला प्रशासन, SAS नगर (मोहाली)। 23 अक्टूबर 2025 से प्रभावी संशोधित कलेक्टर दरों की अधिसूचना।

- द ट्रिब्यून। "मोहाली ने नई कलेक्टर दरें लागू कीं।" 24 अक्टूबर 2025।

- CityNest Realty। "23 अक्टूबर से कलेक्टर दरें बढ़ने पर मोहाली संपत्ति की कीमतें बढ़ेंगी।" 15 अक्टूबर 2025।

- Garah Pravesh। "मोहाली में कलेक्टर दरों में 67% तक की वृद्धि।" नवंबर 2025।

- ClearTax। "आयकर अधिनियम की धारा 50C: भूमि या भवन की बिक्री की करयोग्यता।"

यह लेख मई 2026 तक की सामान्य जानकारी है, कर या कानूनी सलाह नहीं। mohaliaerotropolis.com कर सलाहकार नहीं है। खरीदारों, विक्रेताओं और NRIs को किसी भी विशिष्ट लेन-देन के लिए एक योग्य चार्टर्ड अकाउंटेंट से परामर्श करना चाहिए।

At a glance

Punjab ਦਾ collector rate stamp duty ਲਈ ਇੱਕ floor (ਨੀਵੀਂ ਸੀਮਾ) ਹੈ, ਨਾ ਕਿ market price ਦਾ ਰਿਕਾਰਡ

October 2025 Mohali revision ਨੇ residential rates 20 ਤੋਂ 22% ਵਧਾ ਦਿੱਤੇ, ਅਤੇ gap ਬਰਕਰਾਰ ਹੈ

Section 50C seller ਦੀ deemed sale value ਨੂੰ collector rate 'ਤੇ ਲਾਕ ਕਰ ਦਿੰਦੀ ਹੈ

Section 56(2)(x) buyer 'ਤੇ tax ਲਗਾਉਂਦੀ ਹੈ ਜਦੋਂ registered value SDV ਤੋਂ 10% ਤੋਂ ਵੱਧ ਹੇਠਾਂ ਹੁੰਦੀ ਹੈ

ਵੱਡਾ trap cost basis lock-in ਹੈ ਜੋ resale 'ਤੇ ਮੁਸੀਬਤ ਪੈਦਾ ਕਰਦਾ ਹੈ

Why the gap exists

Collector rate, ਜਿਸਨੂੰ circle rate ਵੀ ਕਿਹਾ ਜਾਂਦਾ ਹੈ, ਉਹ minimum value ਹੈ ਜਿਸ ਤੋਂ ਥੱਲੇ ਕੋਈ ਜਾਇਦਾਦ ਕਾਨੂੰਨੀ ਤੌਰ 'ਤੇ register ਨਹੀਂ ਕੀਤੀ ਜਾ ਸਕਦੀ। ਇਹ stamp duty calculation ਨੂੰ ਨਿਯੰਤ੍ਰਿਤ ਕਰਦੀ ਹੈ, ਅਸਲ market price ਨੂੰ ਨਹੀਂ, ਅਤੇ district administration ਦੁਆਰਾ ਸਾਲਾਨਾ revise ਕੀਤੀ ਜਾਂਦੀ ਹੈ। Mohali ਦਾ ਸਭ ਤੋਂ ਤਾਜ਼ਾ revision 23 October 2025 ਨੂੰ ਲਾਗੂ ਹੋਇਆ, ਜਿਸ ਵਿੱਚ residential rates 20 ਤੋਂ 22% ਅਤੇ industrial rates 30% ਵਧੇ।

Buyer market price ਦਾ ਭੁਗਤਾਨ ਕਰਦਾ ਹੈ ਜਦਕਿ deed 'ਤੇ collector rate register ਹੁੰਦੀ ਹੈ। ਵੇਖਣ ਵਿੱਚ "bचत" stamp duty 'ਤੇ ਹੁੰਦੀ ਹੈ ਜੋ ਘੱਟ number 'ਤੇ calculate ਕੀਤੀ ਜਾਂਦੀ ਹੈ, ਜੋ Punjab ਦੇ 7% rate 'ਤੇ 35% gap 'ਤੇ ਲਗਭਗ ₹2 ਤੋਂ 3 lakh ਬਣਦੀ ਹੈ। ਇਹ figure registration ਸਮੇਂ buyer ਨੂੰ ਦਿਖਾਈ ਜਾਂਦੀ ਹੈ; ਅਸਲ ਲਾਗਤ ਸਾਲਾਂ ਬਾਅਦ ਸਾਹਮਣੇ ਆਉਂਦੀ ਹੈ।

The cost basis trap on resale

ਜਦੋਂ buyer ਆਖਰਕਾਰ ਵੇਚਦਾ ਹੈ, ਤਾਂ capital gains ਲਈ acquisition ਦੀ cost registered purchase price ਹੁੰਦੀ ਹੈ, ਨਾ ਕਿ ਅਸਲ ਵਿੱਚ ਅਦਾ ਕੀਤੀ ਗਈ ਰਕਮ। Income Tax Act paperwork ਨੂੰ ਟਰੈਕ ਕਰਦੀ ਹੈ, ਅਤੇ cash receipts cost ਵਿੱਚ ਨਹੀਂ ਗਿਣੀਆਂ ਜਾਂਦੀਆਂ। ਇਸਦਾ ਮਤਲਬ ਹੈ ਕਿ resale 'ਤੇ capital gain ਘੱਟ registered cost ਤੋਂ calculate ਕੀਤਾ ਜਾਂਦਾ ਹੈ, ਜਿਸ ਨਾਲ ਇੱਕ phantom gain ਪੈਦਾ ਹੁੰਦੀ ਹੈ ਜਿਸ 'ਤੇ seller tax ਅਦਾ ਕਰਦਾ ਹੈ ਭਾਵੇਂ ਅਸਲ ਆਰਥਿਕ gain ਬਹੁਤ ਛੋਟੀ ਹੋਵੇ।

Seller ਨੇ purchase 'ਤੇ stamp duty ਵਿੱਚ ₹2.45 lakh बचाया ਅਤੇ resale 'ਤੇ extra tax ਵਿੱਚ ₹4.37 lakh ਵਾਪਸ ਅਦਾ ਕੀਤਾ, ਉਸੇ ਆਰਥਿਕ gain 'ਤੇ। Break-even seller ਦੇ ਵਿਰੁੱਧ ਹੋ ਗਿਆ ਹੈ, ਅਤੇ cash component ਨੂੰ ਅਜੇ ਵੀ legitimize ਕਰਨ ਦੀ ਲੋੜ ਹੁੰਦੀ ਹੈ ਤਾਂ ਜੋ ਇਸਨੂੰ ਵਰਤਿਆ, banked, ਜਾਂ repatriated ਕੀਤਾ ਜਾ ਸਕੇ।

Section 50C and Section 56(2)(x)

Section 50C of the Income Tax Act seller side 'ਤੇ ਇਸ trap ਨੂੰ ਹੋਰ lock ਕਰ ਦਿੰਦੀ ਹੈ। ਜੇ seller sale ਨੂੰ under-register ਕਰਨ ਦੀ ਕੋਸ਼ਿਸ਼ ਕਰਦਾ ਹੈ ਤਾਂ recorded gain ਛੋਟਾ ਰੱਖਣ ਲਈ, Section 50C actual sale price ਜਾਂ current collector rate ਵਿੱਚੋਂ ਜੋ ਵੱਧ ਹੈ, ਨੂੰ deemed sale consideration ਮੰਨ ਲੈਂਦੀ ਹੈ। Seller exit 'ਤੇ ਵੀ ਉਹੀ understatement ਦੁਹਰਾ ਕੇ gain ਤੋਂ ਨਹੀਂ ਬਚ ਸਕਦਾ।

Section 56(2)(x) buyer ਦਾ mirror image ਹੈ। ਜੇ buyer ਦਾ recorded consideration stamp duty value ਤੋਂ 10% ਤੋਂ ਵੱਧ ਹੇਠਾਂ ਹੈ, ਤਾਂ ਫਰਕ buyer ਦੇ ਹੱਥਾਂ ਵਿੱਚ income from other sources ਵਜੋਂ taxed ਕੀਤਾ ਜਾਂਦਾ ਹੈ। Mohali ਵਿੱਚ ਇਹ rarely apply ਹੁੰਦਾ ਹੈ ਕਿਉਂकि buyers ਠੀਕ collector rate 'ਤੇ register ਕਰਦੇ ਹਨ, ਪਰ exposure ਉਦੋਂ ਖਤਰਨਾਕ ਹੋ ਜਾਂਦਾ ਹੈ ਜਦੋਂ collector rates sharply move ਕਰਦੀਆਂ ਹਨ, ਜਿਵੇਂ October 2025 ਵਿੱਚ।

The NRI angle

NRI sellers ਲਈ, trap ਹੋਰ ਵੀ ਗੰਭੀਰ ਹੋ ਜਾਂਦਾ ਹੈ। TDS under Section 195 long-term capital assets 'ਤੇ ਪੂਰੀ sale consideration ਦੇ 20% 'ਤੇ deducted ਕੀਤਾ ਜਾਂਦਾ ਹੈ, plus surcharge and cess, ਨਾ ਕਿ ਸਿਰਫ gain 'ਤੇ। ਘੱਟ registered cost ਦਾ ਮਤਲਬ ਹੈ ਉੱਚ computed gain, ਛੋਟਾ refund, ਅਤੇ ਹੌਲੀ repatriation, ਕਿਉਂकि banks cash portion ਨੂੰ CA-certified Form 15CB ਤੋਂ ਬਿਨਾਂ remit ਨਹੀਂ ਕਰਨਗੀਆਂ ਜੋ funds ਦਾ source ਦਿਖਾਉਂਦਾ ਹੈ।

The practical path

Actual transaction value 'ਤੇ register ਕਰਨ ਨਾਲ ਅੱਜ stamp duty ਦਾ ਵੱਧ bill ਆਉਂਦਾ ਹੈ, ਪਰ trap ਪੂਰੀ ਤਰ੍ਹਾਂ ਖਤਮ ਹੋ ਜਾਂਦਾ ਹੈ ਅਤੇ ਆਮ ਤੌਰ 'ਤੇ first holding period ਦੇ ਅੰਦਰ break-even ਹੁੰਦਾ ਹੈ। Bank finance ਵਰਤਣ ਵਾਲੇ buyers ਲਈ ਇਹ ਸਵਾਲ ਅਮਲ ਵਿੱਚ rarely ਉਠਦਾ ਹੈ, ਕਿਉਂकि lenders ਸਿਰਫ registered value ਦੇ ਵਿਰੁੱਧ disbursement ਕਰਦੇ ਹਨ, ਕਿਸੇ side cash arrangement ਦੇ ਵਿਰੁੱਧ ਨਹੀਂ।

ਅੱਜ stamp duty ਵਿੱਚ ₹2-3 lakh ਜ਼ਿਆਦਾ

Resale 'ਤੇ capital gains tax ਵਿੱਚ ₹4-5 lakh ਘੱਟ

NRIs ਲਈ normal banking channels ਰਾਹੀਂ clean repatriation

Cash component ਨੂੰ handle, store, ਜਾਂ explain ਕਰਨ ਦੀ ਕੋਈ ਲੋੜ ਨਹੀਂ

Back end 'ਤੇ Section 148 scrutiny risk ਨਹੀਂ

Bottom line

Mohali registry value market price ਨਹੀਂ ਹੈ। Collector rate stamp duty ਲਈ floor ਹੈ, ਨਾ ਕਿ exchange ਹੋਏ ਪੈਸੇ ਦਾ record, ਅਤੇ registration 'ਤੇ ਜੋ बचाया ਜਾਂਦਾ ਹੈ, ਉਹ ਆਮ ਤੌਰ 'ਤے resale 'ਤੇ cash layer ਅਤے audit risk ਨਾਲ ਵਾਪਸ ਅਦਾ ਕੀਤਾ ਜਾਂਦਾ ਹੈ।

Sources

Income Tax Act, 1961. Section 50C, Section 56(2)(x), Section 195. Government of India.

Punjab Stamp Act and Indian Registration Act, 1908.

District Administration, SAS Nagar (Mohali). Notification of revised collector rates effective 23 October 2025.

The Tribune. "Mohali implements new collector rates." 24 October 2025.

CityNest Realty. "Mohali Property Prices to Increase as Collector Rates Rise from October 23." 15 October 2025.

Garah Pravesh. "Collector Rates Hiked up to 67% in Mohali." November 2025.

ClearTax. "Section 50C of Income Tax Act: Taxability of Sale of Land or Building."

This article is general information as of May 2026, not tax or legal advice. mohaliaerotropolis.com is not a tax adviser. Buyers, sellers, and NRIs should consult a qualified chartered accountant for any specific transaction.