The Price Gradient Is Widening

Mohali's property market in 2026 is not one market. It is at least three, running at different speeds and with different risk profiles, and the distance between them is growing.

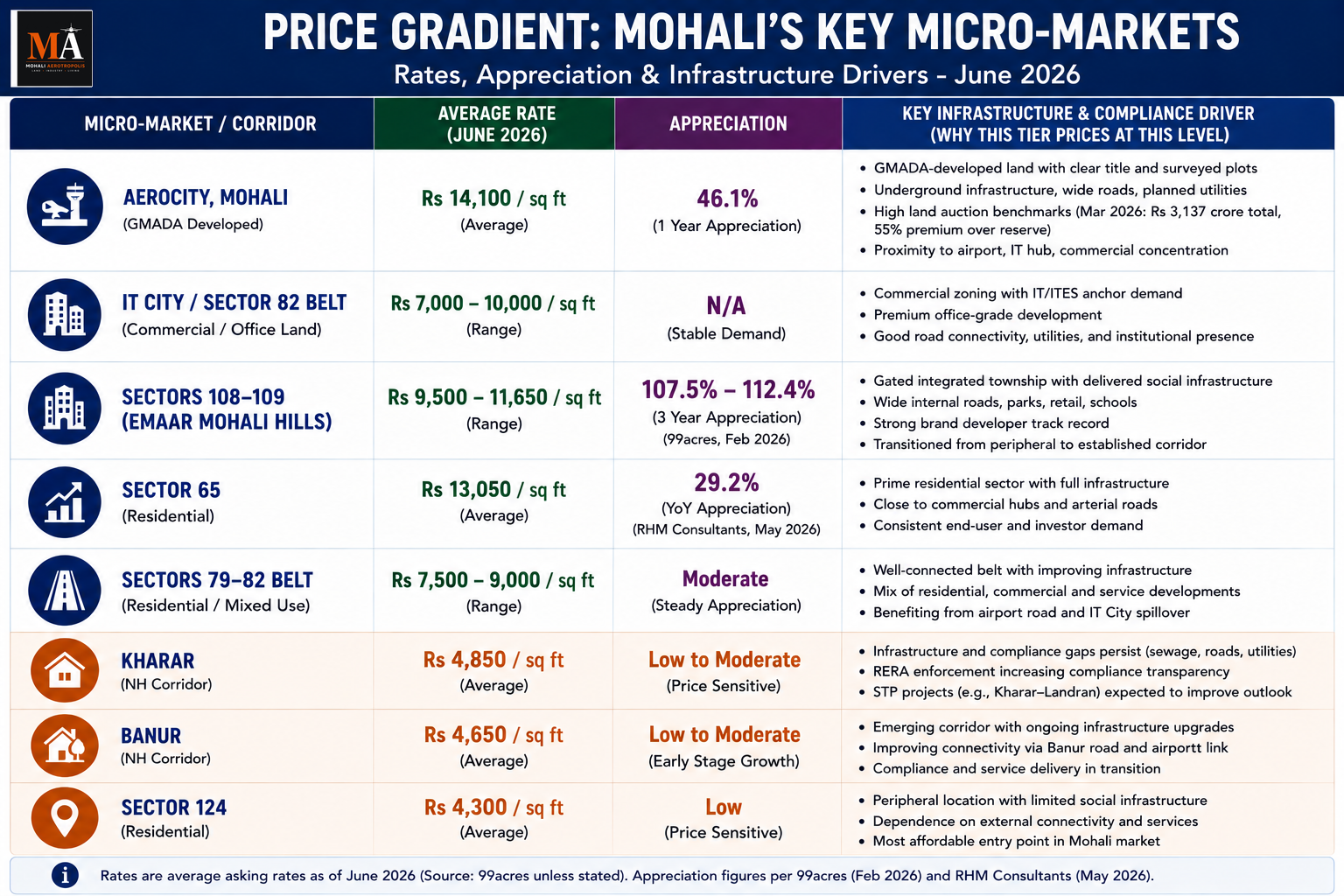

At the established end: Aerocity land rates average Rs 14,100 per square foot on 99acres. IT City office-grade land trades in the Rs 7,000 to Rs 10,000 per square foot band. The March 2026 GMADA auction produced Rs 3,137 crore in revenue, with a single Aerocity housing site fetching Rs 311.74 crore for 6.19 acres, with the auction as a whole exceeding the reserve price by 55 percent. Sectors 108 and 109 (Emaar Mohali Hills) have appreciated 107.5 to 112.4 percent over three years per 99acres February 2026 data. Sector 65 delivered 29.2 percent year-on-year appreciation per the Realty Holding and Management Consultants May 2026 report.

At the affordable end: Kharar averages Rs 4,850 per square foot. Banur is at Rs 4,650. Sector 124 is at Rs 4,300. Sector 92, which sits between the two belts geographically, is at Rs 5,800. For buyers whose budget puts them in the sub-Rs 1 crore category, these are the corridors where the supply exists.

The spread between Aerocity and Kharar, roughly Rs 10,000 per square foot at current averages, is not new. But it is wider than it was three years ago, and understanding why it is widening matters more than the number itself.

Why the Established Corridor Keeps Pulling Ahead

The appreciation in Aerocity, IT City, and the Airport Road belt is not speculation untethered from fundamentals. It is driven by a specific set of infrastructure and regulatory conditions that the affordable peripheral belt does not yet share.

GMADA-developed land in Aerocity comes with surveyed plots, confirmed legal title, underground utilities, planned road widths, and an authority that processes transfers and mutations in a documented way. The buyer of an Aerocity plot knows exactly what they are buying and can verify it through GMADA's own records. That certainty is priced in.

The peripheral corridor — Kharar, Banur, Sunny Enclave, the NH-adjacent developments — has a much more varied compliance picture. From what has been documented this month alone: borewells being used for sewage disposal instead of STPs in Bhagomajra; the Kharar-Landran road excavated for PWSSB sewerage work and not restored; JTPL Sector 115 under PPCB show-cause for non-functional sewage infrastructure; multiple housing societies in Rani Majra, Togan, and Palheri discharging into seasonal rivulets. These are not isolated incidents. They are a pattern of infrastructure delivery gaps that affect the day-to-day liveability of properties in these corridors, and that pattern is reflected in their pricing.

What RERA Enforcement Is Doing in the Peripheral Belt

The framing of a "regulatory squeeze" from RERA on peripheral areas is partially accurate but worth unpacking. RERA enforcement in the Kharar corridor and the NH-adjacent developments is not arbitrary pressure on affordable buyers. It is the systematic closure of the gap between what was sold and what was built.

Punjab RERA has been issuing notices under Section 59 against projects that should have been registered and were not. It has been enforcing refund orders against developers who took deposits and did not deliver. The Bajwa Developers May 2026 order, the consumer commission's Amar Pal versus RKM Housing ruling, and the mounting GMADA dues enforcement list all represent the same dynamic: developers in the peripheral market who operated with informal or under-disclosed practices are being brought into a compliance framework that was absent when they launched.

For buyers who are already in these projects, that enforcement is protective — it gives them legal recourse they previously lacked. For developers who have been operating without full compliance, it is a squeeze. The two things look the same from outside but have very different implications for who benefits.

The Structural Explanation, Not the Simple One

The luxury-versus-affordable framing implies that the market is splitting along income lines — that rich buyers get the appreciation and budget buyers get the regulation. The actual split is along infrastructure and legal compliance lines, and those do not map perfectly onto income levels.

A buyer who purchased in an Aerocity GMADA scheme ten years ago at allotment price was not a luxury buyer in income terms. They were buying at collector-rate pricing, which the Realty Consultants May 2026 report describes as structurally below open market transacted prices. What made that purchase produce strong appreciation was not their income level — it was that the product they bought came with GMADA infrastructure delivery, legal title clarity, and a regulatory framework that held through multiple administrations.

A buyer who purchased in a peripheral Kharar project at a lower price point did not necessarily get a worse deal in income terms. What they got was more regulatory uncertainty, infrastructure that depends on the developer's delivery capability, and legal recourse that was weaker before RERA and better now.

The convergence that is happening — RERA enforcement bringing peripheral projects into compliance, GMADA infrastructure contracting expanding toward the Banur and Kharar belts, the Kharar-Landran STP expected to commission in July — is the mechanism through which some of that price gap eventually closes. It does not close quickly, and it does not close uniformly. But it does close, as the outer arc appreciation story in Sectors 108, 109, and 114 demonstrates.

Three years ago those sectors were the peripheral market. They are not anymore.

---

Sources

- 99acres — Property rates and price trends, Aerocity Mohali, Kharar, Banur, Sector 92, June 2026

- 99acres — Most appreciated localities Mohali, February 2026 (Sector 108: 112.4%, Sector 109: 107.5% over three years)

- Realty Holding and Management Consultants — Property rates Mohali 2026 ground-level report, May 14, 2026

- GMADA March 2026 auction results — Rs 3,137 crore, 55% premium over reserve, Aerocity housing site Rs 311.74 crore

- Mohali Aerotropolis — RERA enforcement coverage and PPCB sewage cases, June 2026

मूल्य अंतर बढ़ता जा रहा है

मोहाली का प्रॉपर्टी बाजार 2026 में एक बाजार नहीं है। यह कम से कम तीन बाजार हैं, जो अलग-अलग गति से चल रहे हैं और जिनके जोखिम प्रोफाइल अलग हैं, और इनके बीच की दूरी बढ़ती जा रही है।

स्थापित छोर पर: एरोसिटी में जमीन की दरें 99acres पर औसतन 14,100 रुपये प्रति वर्ग फुट हैं। IT City में ऑफिस-ग्रेड जमीन 7,000 से 10,000 रुपये प्रति वर्ग फुट के दायरे में कारोबार करती है। मार्च 2026 की GMADA नीलामी ने 3,137 करोड़ रुपये का राजस्व उत्पन्न किया, जिसमें एरोसिटी का एक हाउसिंग प्लॉट 6.19 एकड़ के लिए 311.74 करोड़ रुपये में बिका, और पूरी नीलामी ने आरक्षित मूल्य से 55 प्रतिशत अधिक कीमत हासिल की। 99acres के फरवरी 2026 के आंकड़ों के अनुसार, सेक्टर 108 और 109 (एमर मोहाली हिल्स) में तीन वर्षों में 107.5 से 112.4 प्रतिशत की वृद्धि हुई है। रियल्टी होल्डिंग एंड मैनेजमेंट कंसल्टेंट्स की मई 2026 की रिपोर्ट के अनुसार, सेक्टर 65 में 29.2 प्रतिशत सालाना वृद्धि दर्ज की गई।

किफायती छोर पर: खरड़ में औसत दर 4,850 रुपये प्रति वर्ग फुट है। बनूर में 4,650 रुपये प्रति वर्ग फुट है। सेक्टर 124 में 4,300 रुपये प्रति वर्ग फुट है। सेक्टर 92, जो भौगोलिक रूप से दोनों पट्टियों के बीच स्थित है, 5,800 रुपये प्रति वर्ग फुट पर है। जिन खरीदारों का बजट 1 करोड़ रुपये से कम की श्रेणी में आता है, उनके लिए ये वे गलियारे हैं जहां आपूर्ति मौजूद है।

एरोसिटी और खरड़ के बीच का अंतर, वर्तमान औसत पर लगभग 10,000 रुपये प्रति वर्ग फुट, नया नहीं है। लेकिन यह तीन साल पहले की तुलना में अधिक है, और यह समझना कि यह अंतर क्यों बढ़ रहा है, इस संख्या से अधिक मायने रखता है।

स्थापित गलियारा क्यों आगे बढ़ता जा रहा है

एरोसिटी, IT City और एयरपोर्ट रोड पट्टी में वृद्धि बुनियादी सिद्धांतों से रहित अटकलबाजी नहीं है। यह बुनियादी ढांचे और नियामक स्थितियों के एक विशिष्ट सेट द्वारा संचालित है, जो किफायती परिधीय पट्टी में अभी तक मौजूद नहीं है।

एरोसिटी में GMADA द्वारा विकसित जमीन सर्वेक्षित प्लॉटों, पुष्ट कानूनी शीर्षक, भूमिगत उपयोगिताओं, नियोजित सड़क चौड़ाई और एक ऐसे प्राधिकरण के साथ आती है जो हस्तांतरण और उत्परिवर्तन को दस्तावेजी तरीके से संसाधित करता है। एरोसिटी प्लॉट का खरीदार जानता है कि वे वास्तव में क्या खरीद रहे हैं और GMADA के अपने रिकॉर्ड के माध्यम से इसे सत्यापित कर सकते हैं। वह निश्चितता मूल्य में शामिल है।

परिधीय गलियारा — खरड़, बनूर, सनी एन्क्लेव, NH-सटे विकास — में अनुपालन की तस्वीर कहीं अधिक विविध है। अकेले इसी महीने दस्तावेजीकृत किए गए मामलों से: भगोमाजरा में STPs के बजाय सीवेज निपटान के लिए बोरवेल का उपयोग; PWSSB सीवरेज कार्य के लिए खरड़-लांडरां सड़क की खुदाई और उसकी बहाली न होना; गैर-कार्यात्मक सीवेज बुनियादी ढांचे के लिए PPCB के शो-कॉज के तहत JTPL सेक्टर 115; रानी माजरा, तोगन और पलेहरी में कई हाउसिंग सोसाइटियां मौसमी नालों में निर्वहन कर रही हैं। ये अलग-थलग घटनाएं नहीं हैं। ये बुनियादी ढांचा वितरण में कमियों का एक पैटर्न हैं, जो इन गलियारों में संपत्तियों की दैनिक रहने योग्यता को प्रभावित करते हैं, और वह पैटर्न उनकी कीमतों में परिलक्षित होता है।

परिधीय पट्टी में RERA प्रवर्तन क्या कर रहा है

परिधीय क्षेत्रों पर RERA से "नियामक दबाव" का ढांचा आंशिक रूप से सटीक है, लेकिन इसे समझना आवश्यक है। खरड़ गलियारे और NH-सटे विकासों में RERA प्रवर्तन किफायती खरीदारों पर मनमाना दबाव नहीं है। यह जो बेचा गया था और जो बनाया गया था, उसके बीच के अंतर को व्यवस्थित रूप से बंद करना है।

पंजाब RERA ने उन परियोजनाओं के खिलाफ धारा 59 के तहत नोटिस जारी किए हैं जिन्हें पंजीकृत किया जाना चाहिए था और नहीं किया गया। इसने उन डेवलपर्स के खिलाफ रिफंड आदेश लागू किए हैं जिन्होंने जमा राशि ली और डिलीवरी नहीं की। बाजवा डेवलपर्स का मई 2026 का आदेश, उपभोक्ता आयोग का अमर पाल बनाम RKM हाउसिंग का फैसला, और GMADA बकाया प्रवर्तन सूची का बढ़ता दबाव सभी एक ही गतिशीलता का प्रतिनिधित्व करते हैं: परिधीय बाजार में डेवलपर्स जो अनौपचारिक या गैर-प्रकट प्रथाओं के साथ काम करते थे, उन्हें एक अनुपालन ढांचे में लाया जा रहा है जो उनके लॉन्च के समय अनुपस्थित था।

उन खरीदारों के लिए जो पहले से ही इन परियोजनाओं में हैं, वह प्रवर्तन सुरक्षात्मक है — यह उन्हें कानूनी सहारा देता है जो पहले उनके पास नहीं था। उन डेवलपर्स के लिए जो पूर्ण अनुपालन के बिना काम कर रहे हैं, यह एक दबाव है। ये दो चीजें बाहर से एक जैसी दिखती हैं, लेकिन उनके बहुत अलग निहितार्थ हैं कि किसे लाभ होता है।

संरचनात्मक व्याख्या, सरल नहीं

लक्जरी-बनाम-किफायती ढांचा यह दर्शाता है कि बाजार आय स्तरों के साथ विभाजित हो रहा है — कि अमीर खरीदारों को वृद्धि मिलती है और बजट खरीदारों को विनियमन मिलता है। वास्तविक विभाजन बुनियादी ढांचे और कानूनी अनुपालन रेखाओं के साथ है, और ये आय स्तरों पर पूरी तरह से मेल नहीं खाते हैं।

एक खरीदार जिसने दस साल पहले आवंटन मूल्य पर एरोसिटी की GMADA योजना में खरीदा था, वह आय के मामले में लक्जरी खरीदार नहीं था। वे कलेक्टर-दर मूल्य पर खरीद रहे थे, जिसे रियल्टी कंसल्टेंट्स की मई 2026 की रिपोर्ट संरचनात्मक रूप से खुले बाजार के लेन-देन मूल्य से नीचे बताती है। उस खरीद को मजबूत वृद्धि उत्पन्न करने वाली बनाने वाली चीज उनका आय स्तर नहीं था — यह था कि उन्होंने जो उत्पाद खरीदा वह GMADA बुनियादी ढांचा वितरण, कानूनी शीर्षक स्पष्टता और एक नियामक ढांचे के साथ आया जो कई प्रशासनों में कायम रहा।

एक खरीदार जिसने कम मूल्य बिंदु पर एक परिधीय खरड़ परियोजना में खरीदा, उसे जरूरी नहीं कि आय के मामले में बुरा सौदा मिला। उन्हें जो मिला वह अधिक नियामक अनिश्चितता थी, बुनियादी ढांचा जो डेवलपर की डिलीवरी क्षमता पर निर्भर करता है, और कानूनी सहारा जो RERA से पहले कमजोर था और अब बेहतर है।

जो अभिसरण हो रहा है — RERA प्रवर्तन परिधीय परियोजनाओं को अनुपालन में ला रहा है, GMADA बुनियादी ढांचा अनुबंध बनूर और खरड़ पट्टियों की ओर विस्तार कर रहा है, खरड़-लांडरां STP के जुलाई में चालू होने की उम्मीद है — वह वह तंत्र है जिसके माध्यम से कीमतों में कुछ अंतर अंततः बंद होता है। यह जल्दी बंद नहीं होता, और यह एक समान रूप से बंद नहीं होता। लेकिन यह बंद होता है, जैसा कि सेक्टर 108, 109 और 114 में बाहरी चाप वृद्धि की कहानी प्रदर्शित करती है।

तीन साल पहले वे सेक्टर परिधीय बाजार थे। वे अब नहीं हैं।

---

स्रोत

- 99acres — प्रॉपर्टी दरें और मूल्य रुझान, एरोसिटी मोहाली, खरड़, बनूर, सेक्टर 92, जून 2026

- 99acres — मोहाली के सबसे अधिक सराहे गए इलाके, फरवरी 2026 (सेक्टर 108: 112.4%, सेक्टर 109: 107.5% तीन वर्षों में)

- रियल्टी होल्डिंग एंड मैनेजमेंट कंसल्टेंट्स — मोहाली 2026 में प्रॉपर्टी दरें ग्राउंड-लेवल रिपोर्ट, 14 मई, 2026

- GMADA मार्च 2026 नीलामी परिणाम — 3,137 करोड़ रुपये, आरक्षित मूल्य पर 55% प्रीमियम, एरोसिटी हाउसिंग साइट 311.74 करोड़ रुपये

- मोहाली एरोट्रोपोलिस — RERA प्रवर्तन कवरेज और PPCB सीवेज मामले, जून 2026

ਕੀਮਤ ਦਾ ਅੰਤਰ ਵੱਧ ਰਿਹਾ ਹੈ

ਮੋਹਾਲੀ ਦਾ ਜਾਇਦਾਦ ਬਾਜ਼ਾਰ 2026 ਵਿੱਚ ਇੱਕ ਬਾਜ਼ਾਰ ਨਹੀਂ ਹੈ। ਇਹ ਘੱਟੋ-ਘੱਟ ਤਿੰਨ ਹੈ, ਵੱਖ-ਵੱਖ ਗਤੀਆਂ 'ਤੇ ਚੱਲ ਰਹੇ ਹਨ ਅਤੇ ਵੱਖ-ਵੱਖ ਜੋਖਮ ਪ੍ਰੋਫਾਈਲਾਂ (risk profiles) ਦੇ ਨਾਲ, ਅਤੇ ਉਹਨਾਂ ਵਿਚਕਾਰ ਦੂਰੀ ਵਧ ਰਹੀ ਹੈ।

ਸਥਾਪਿਤ ਸਿਰੇ 'ਤੇ: 99acres 'ਤੇ Aerocity ਜ਼ਮੀਨ ਦੀਆਂ ਦਰਾਂ ਔਸਤਨ Rs 14,100 ਪ੍ਰਤੀ ਵਰਗ ਫੁੱਟ ਹਨ। IT City ਦਫ਼ਤਰ-ਗ੍ਰੇਡ ਜ਼ਮੀਨ Rs 7,000 ਤੋਂ Rs 10,000 ਪ੍ਰਤੀ ਵਰਗ ਫੁੱਟ ਦੇ ਬੈਂਡ (band) ਵਿੱਚ ਵਪਾਰ ਕਰਦੀ ਹੈ। ਮਾਰਚ 2026 ਦੀ GMADA ਨੀਲਾਮੀ ਨੇ Rs 3,137 ਕਰੋੜ ਦਾ ਮਾਲੀਆ ਪੈਦਾ ਕੀਤਾ, ਜਿਸ ਵਿੱਚ Aerocity ਦੇ ਇੱਕ ਹਾਊਸਿੰਗ ਸਾਈਟ ਨੇ 6.19 ਏਕੜ ਲਈ Rs 311.74 ਕਰੋੜ ਪ੍ਰਾਪਤ ਕੀਤੇ, ਅਤੇ ਸਮੁੱਚੀ ਨੀਲਾਮੀ ਰਿਜ਼ਰਵ ਕੀਮਤ (reserve price) ਤੋਂ 55 ਪ੍ਰਤੀਸ਼ਤ ਵੱਧ ਰਹੀ। 99acres ਫਰਵਰੀ 2026 ਦੇ ਅੰਕੜਿਆਂ ਅਨੁਸਾਰ ਸੈਕਟਰ 108 ਅਤੇ 109 (Emaar Mohali Hills) ਤਿੰਨ ਸਾਲਾਂ ਵਿੱਚ 107.5 ਤੋਂ 112.4 ਪ੍ਰਤੀਸ਼ਤ ਤੱਕ ਵਧੇ ਹਨ। Realty Holding and Management Consultants ਮਈ 2026 ਦੀ ਰਿਪੋਰਟ ਅਨੁਸਾਰ ਸੈਕਟਰ 65 ਨੇ 29.2 ਪ੍ਰਤੀਸ਼ਤ ਸਾਲ-ਦਰ-ਸਾਲ ਵਾਧਾ ਦਿੱਤਾ।

ਕਿਫਾਇਤੀ ਸਿਰੇ 'ਤੇ: Kharar ਔਸਤਨ Rs 4,850 ਪ੍ਰਤੀ ਵਰਗ ਫੁੱਟ ਹੈ। Banur Rs 4,650 'ਤੇ ਹੈ। ਸੈਕਟਰ 124 Rs 4,300 'ਤੇ ਹੈ। ਸੈਕਟਰ 92, ਜੋ ਭੂਗੋਲਿਕ ਤੌਰ 'ਤੇ ਦੋਵਾਂ ਪੱਟੀਆਂ (belts) ਦੇ ਵਿਚਕਾਰ ਸਥਿਤ ਹੈ, Rs 5,800 'ਤੇ ਹੈ। ਉਹਨਾਂ ਖਰੀਦਦਾਰਾਂ ਲਈ ਜਿਨ੍ਹਾਂ ਦਾ ਬਜਟ ਉਹਨਾਂ ਨੂੰ sub-Rs 1 ਕਰੋੜ ਸ਼੍ਰੇਣੀ ਵਿੱਚ ਰੱਖਦਾ ਹੈ, ਇਹ ਉਹ ਗਲਿਆਰੇ (corridors) ਹਨ ਜਿੱਥੇ ਸਪਲਾਈ (supply) ਮੌਜੂਦ ਹੈ।

Aerocity ਅਤੇ Kharar ਵਿਚਕਾਰ ਫੈਲਾਅ (spread), ਮੌਜੂਦਾ ਔਸਤਨ Rs 10,000 ਪ੍ਰਤੀ ਵਰਗ ਫੁੱਟ, ਨਵਾਂ ਨਹੀਂ ਹੈ। ਪਰ ਇਹ ਤਿੰਨ ਸਾਲ ਪਹਿਲਾਂ ਨਾਲੋਂ ਵਿਆਪਕ (wider) ਹੈ, ਅਤੇ ਇਹ ਸਮਝਣਾ ਕਿ ਇਹ ਕਿਉਂ ਵਧ ਰਿਹਾ ਹੈ, ਸੰਖਿਆ (number) ਤੋਂ ਵੱਧ ਮਹੱਤਵਪੂਰਨ ਹੈ।

ਸਥਾਪਿਤ ਗਲਿਆਰਾ (Established Corridor) ਕਿਉਂ ਅੱਗੇ ਵਧਦਾ ਰਹਿੰਦਾ ਹੈ

Aerocity, IT City, ਅਤੇ Airport Road ਪੱਟੀ (belt) ਵਿੱਚ ਵਾਧਾ (appreciation) ਬੁਨਿਆਦੀ ਤੱਤਾਂ (fundamentals) ਤੋਂ ਅਣਜੁੜੀ ਅਟਕਲਾਂ (speculation) ਨਹੀਂ ਹੈ। ਇਹ ਬੁਨਿਆਦੀ ਢਾਂਚੇ (infrastructure) ਅਤੇ ਰੈਗੂਲੇਟਰੀ (regulatory) ਸਥਿਤੀਆਂ ਦੇ ਇੱਕ ਖਾਸ ਸਮੂਹ ਦੁਆਰਾ ਚਲਾਇਆ ਜਾਂਦਾ ਹੈ ਜੋ ਕਿਫਾਇਤੀ ਬਾਹਰੀ (peripheral) ਪੱਟੀ ਅਜੇ ਤੱਕ ਸਾਂਝਾ ਨਹੀਂ ਕਰਦੀ।

Aerocity ਵਿੱਚ GMADA-ਵਿਕਸਿਤ ਜ਼ਮੀਨ ਸਰਵੇਖਣ ਕੀਤੇ ਪਲਾਟਾਂ (surveyed plots), ਪੁਸ਼ਟੀ ਕੀਤੇ ਕਾਨੂੰਨੀ ਸਿਰਲੇਖ (confirmed legal title), ਭੂਮੀਗਤ ਉਪਯੋਗਤਾਵਾਂ (underground utilities), ਯੋਜਨਾਬੱਧ ਸੜਕਾਂ ਦੀ ਚੌੜਾਈ (planned road widths), ਅਤੇ ਇੱਕ ਅਥਾਰਟੀ (authority) ਦੇ ਨਾਲ ਆਉਂਦੀ ਹੈ ਜੋ ਤਬਾਦਲੇ (transfers) ਅਤੇ ਮਿਊਟੇਸ਼ਨਾਂ (mutations) ਨੂੰ ਦਸਤਾਵੇਜ਼ੀ (documented) ਤਰੀਕੇ ਨਾਲ ਪ੍ਰਕਿਰਿਆ ਕਰਦੀ ਹੈ। Aerocity ਪਲਾਟ ਦਾ ਖਰੀਦਦਾਰ ਜਾਣਦਾ ਹੈ ਕਿ ਉਹ ਅਸਲ ਵਿੱਚ ਕੀ ਖਰੀਦ ਰਿਹਾ ਹੈ ਅਤੇ GMADA ਦੇ ਆਪਣੇ ਰਿਕਾਰਡਾਂ ਰਾਹੀਂ ਇਸਦੀ ਪੁਸ਼ਟੀ ਕਰ ਸਕਦਾ ਹੈ। ਉਹ ਨਿਸ਼ਚਤਤਾ (certainty) ਕੀਮਤ ਵਿੱਚ ਸ਼ਾਮਲ ਹੈ।

ਬਾਹਰੀ ਗਲਿਆਰਾ (peripheral corridor) — Kharar, Banur, Sunny Enclave, NH-ਨਾਲ ਲਗਦੇ ਵਿਕਾਸ (developments) — ਦੀ ਪਾਲਣਾ (compliance) ਦੀ ਤਸਵੀਰ ਬਹੁਤ ਜ਼ਿਆਦਾ ਵਿਭਿੰਨ (varied) ਹੈ। ਇਸ ਮਹੀਨੇ ਹੀ ਦਸਤਾਵੇਜ਼ੀ ਕੀਤੇ ਗਏ ਤੋਂ: Bhagomajra ਵਿੱਚ STPs ਦੀ ਬਜਾਏ ਸੀਵਰੇਜ ਨਿਪਟਾਰੇ ਲਈ ਬੋਰਵੈੱਲ (borewells) ਵਰਤੇ ਜਾ ਰਹੇ ਹਨ; PWSSB ਸੀਵਰੇਜ ਦੇ ਕੰਮ ਲਈ ਖੋਦੀ ਗਈ Kharar-Landran ਸੜਕ ਮੁਰੰਮਤ ਨਹੀਂ ਕੀਤੀ ਗਈ; JTPL ਸੈਕਟਰ 115 ਗੈਰ-ਕਾਰਜਸ਼ੀਲ ਸੀਵਰੇਜ ਬੁਨਿਆਦੀ ਢਾਂਚੇ ਲਈ PPCB ਦੇ ਸ਼ੋ-ਕਾਜ਼ (show-cause) ਅਧੀਨ ਹੈ; Rani Majra, Togan, ਅਤੇ Palheri ਵਿੱਚ ਕਈ ਹਾਊਸਿੰਗ ਸੁਸਾਇਟੀਆਂ ਮੌਸਮੀ ਨਦੀਆਂ (seasonal rivulets) ਵਿੱਚ ਛੱਡ ਰਹੀਆਂ ਹਨ। ਇਹ ਵੱਖ-ਵੱਖ ਘਟਨਾਵਾਂ (isolated incidents) ਨਹੀਂ ਹਨ। ਇਹ ਬੁਨਿਆਦੀ ਢਾਂਚੇ ਦੀ ਡਿਲੀਵਰੀ (infrastructure delivery) ਵਿੱਚ ਪਾੜੇ (gaps) ਦਾ ਇੱਕ ਪੈਟਰਨ (pattern) ਹਨ ਜੋ ਇਹਨਾਂ ਗਲਿਆਰਿਆਂ (corridors) ਵਿੱਚ ਜਾਇਦਾਦਾਂ ਦੀ ਰੋਜ਼ਾਨਾ ਰਹਿਣਯੋਗਤਾ (liveability) ਨੂੰ ਪ੍ਰਭਾਵਿਤ ਕਰਦੇ ਹਨ, ਅਤੇ ਉਹ ਪੈਟਰਨ ਉਹਨਾਂ ਦੀ ਕੀਮਤ ਨਿਰਧਾਰਨ (pricing) ਵਿੱਚ ਪ੍ਰਤੀਬਿੰਬਤ ਹੁੰਦਾ ਹੈ।

ਬਾਹਰੀ ਪੱਟੀ (Peripheral Belt) ਵਿੱਚ RERA ਲਾਗੂਕਰਨ (Enforcement) ਕੀ ਕਰ ਰਿਹਾ ਹੈ

ਬਾਹਰੀ ਖੇਤਰਾਂ (peripheral areas) 'ਤੇ RERA ਤੋਂ "ਰੈਗੂਲੇਟਰੀ ਦਬਾਅ" (regulatory squeeze) ਦਾ ਢਾਂਚਾ (framing) ਅੰਸ਼ਕ ਤੌਰ 'ਤੇ ਸਹੀ ਹੈ ਪਰ ਇਸਨੂੰ ਖੋਲ੍ਹਣਾ (unpack) ਯੋਗ ਹੈ। Kharar ਗਲਿਆਰੇ (corridor) ਅਤੇ NH-ਨਾਲ ਲਗਦੇ ਵਿਕਾਸ (developments) ਵਿੱਚ RERA ਲਾਗੂ ਕਰਨਾ (enforcement) ਕਿਫਾਇਤੀ ਖਰੀਦਦਾਰਾਂ 'ਤੇ ਮਨਮਾਨੀ (arbitrary) ਦਬਾਅ ਨਹੀਂ ਹੈ। ਇਹ ਉਸ ਪਾੜੇ (gap) ਦਾ ਯੋਜਨਾਬੱਧ (systematic) ਬੰਦ ਕਰਨਾ (closure) ਹੈ ਜੋ ਵੇਚਿਆ ਗਿਆ ਸੀ ਅਤੇ ਜੋ ਬਣਾਇਆ ਗਿਆ ਸੀ, ਦੇ ਵਿਚਕਾਰ।

ਪੰਜਾਬ RERA ਉਹਨਾਂ ਪ੍ਰਾਜੈਕਟਾਂ (projects) ਦੇ ਵਿਰੁੱਧ ਧਾਰਾ 59 (Section 59) ਦੇ ਅਧੀਨ ਨੋਟਿਸ (notices) ਜਾਰੀ ਕਰ ਰਿਹਾ ਹੈ ਜਿਨ੍ਹਾਂ ਨੂੰ ਰਜਿਸਟਰ (registered) ਹੋਣਾ ਚਾਹੀਦਾ ਸੀ ਅਤੇ ਨਹੀਂ ਹੋਇਆ। ਇਹ ਉਹਨਾਂ ਡਿਵੈਲਪਰਾਂ (developers) ਦੇ ਵਿਰੁੱਧ ਰਿਫੰਡ (refund) ਆਦੇਸ਼ (orders) ਲਾਗੂ ਕਰ ਰਿਹਾ ਹੈ ਜਿਨ੍ਹਾਂ ਨੇ ਜਮ੍ਹਾਂ (deposits) ਲਏ ਅਤੇ ਡਿਲੀਵਰ (deliver) ਨਹੀਂ ਕੀਤਾ। Bajwa Developers ਮਈ 2026 ਦਾ ਆਦੇਸ਼, ਖਪਤਕਾਰ ਕਮਿਸ਼ਨ (consumer commission) ਦਾ Amar Pal ਬਨਾਮ RKM Housing ਦਾ ਫੈਸਲਾ, ਅਤੇ ਵਧਦੀ GMADA ਡਿਊਜ਼ (dues) ਲਾਗੂ ਕਰਨ ਦੀ ਸੂਚੀ (enforcement list) ਸਾਰੇ ਇੱਕੋ ਗਤੀਸ਼ੀਲਤਾ (dynamic) ਨੂੰ ਦਰਸਾਉਂਦੇ ਹਨ: ਬਾਹਰੀ (peripheral) ਬਾਜ਼ਾਰ ਵਿੱਚ ਡਿਵੈਲਪਰ ਜੋ ਅਨੌਪਚਾਰਿਕ (informal) ਜਾਂ ਘੱਟ-ਖੁਲਾਸੇ (under-disclosed) ਅਭਿਆਸਾਂ (practices) ਨਾਲ ਕੰਮ ਕਰਦੇ ਸਨ, ਉਹਨਾਂ ਨੂੰ ਇੱਕ ਪਾਲਣਾ ਢਾਂਚੇ (compliance framework) ਵਿੱਚ ਲਿਆਂਦਾ ਜਾ ਰਿਹਾ ਹੈ ਜੋ ਉਹਨਾਂ ਦੇ ਲਾਂਚ (launch) ਕਰਨ ਵੇਲੇ ਗੈਰ-ਹਾਜ਼ਰ (absent) ਸੀ।

ਉਹਨਾਂ ਖਰੀਦਦਾਰਾਂ ਲਈ ਜੋ ਪਹਿਲਾਂ ਹੀ ਇਹਨਾਂ ਪ੍ਰਾਜੈਕਟਾਂ (projects) ਵਿੱਚ ਹਨ, ਉਹ ਲਾਗੂਕਰਨ (enforcement) ਸੁਰੱਖਿਆਤਮਕ (protective) ਹੈ — ਇਹ ਉਹਨਾਂ ਨੂੰ ਕਾਨੂੰਨੀ ਨਿਵਾਰਣ (legal recourse) ਦਿੰਦਾ ਹੈ ਜਿਸਦੀ ਉਹਨਾਂ ਕੋਲ ਪਹਿਲਾਂ ਘਾਟ ਸੀ। ਉਹਨਾਂ ਡਿਵੈਲਪਰਾਂ ਲਈ ਜੋ ਪੂਰੀ ਪਾਲਣਾ (full compliance) ਤੋਂ ਬਿਨਾਂ ਕੰਮ ਕਰ ਰਹੇ ਹਨ, ਇਹ ਇੱਕ ਦਬਾਅ (squeeze) ਹੈ। ਦੋਵੇਂ ਚੀਜ਼ਾਂ ਬਾਹਰੋਂ ਇੱਕੋ ਜਿਹੀਆਂ ਲੱਗਦੀਆਂ ਹਨ ਪਰ ਇਸ ਗੱਲ ਦੇ ਬਹੁਤ ਵੱਖ-ਵੱਖ ਪ੍ਰਭਾਵ (implications) ਹਨ ਕਿ ਕਿਸ ਨੂੰ ਲਾਭ ਹੁੰਦਾ ਹੈ।

ਢਾਂਚਾਗਤ ਵਿਆਖਿਆ (Structural Explanation), ਸਧਾਰਨ ਨਹੀਂ

ਲਗਜ਼ਰੀ-ਬਨਾਮ-ਕਿਫਾਇਤੀ (luxury-versus-affordable) ਢਾਂਚਾ (framing) ਇਹ ਦਰਸਾਉਂਦਾ ਹੈ ਕਿ ਬਾਜ਼ਾਰ ਆਮਦਨ (income) ਦੀਆਂ ਲਾਈਨਾਂ ਦੇ ਨਾਲ ਵੰਡ ਰਿਹਾ ਹੈ — ਕਿ ਅਮੀਰ ਖਰੀਦਦਾਰਾਂ ਨੂੰ ਵਾਧਾ (appreciation) ਮਿਲਦਾ ਹੈ ਅਤੇ ਬਜਟ ਖਰੀਦਦਾਰਾਂ ਨੂੰ ਰੈਗੂਲੇਸ਼ਨ (regulation) ਮਿਲਦਾ ਹੈ। ਅਸਲ ਵੰਡ (actual split) ਬੁਨਿਆਦੀ ਢਾਂਚੇ (infrastructure) ਅਤੇ ਕਾਨੂੰਨੀ ਪਾਲਣਾ (legal compliance) ਦੀਆਂ ਲਾਈਨਾਂ ਦੇ ਨਾਲ ਹੈ, ਅਤੇ ਉਹ ਆਮਦਨ ਦੇ ਪੱਧਰਾਂ (income levels) 'ਤੇ ਪੂਰੀ ਤਰ੍ਹਾਂ ਮੈਪ (map) ਨਹੀਂ ਹੁੰਦੇ।

ਇੱਕ ਖਰੀਦਦਾਰ ਜਿਸਨੇ ਦਸ ਸਾਲ ਪਹਿਲਾਂ GMADA Aerocity ਸਕੀਮ (scheme) ਵਿੱਚ ਅਲਾਟਮੈਂਟ (allotment) ਕੀਮਤ 'ਤੇ ਖਰੀਦਿਆ ਸੀ, ਉਹ ਆਮਦਨ ਦੇ ਲਿਹਾਜ਼ ਨਾਲ ਲਗਜ਼ਰੀ ਖਰੀਦਦਾਰ ਨਹੀਂ ਸੀ। ਉਹ ਕੁਲੈਕਟਰ-ਰੇਟ (collector-rate) ਕੀਮਤ 'ਤੇ ਖਰੀਦ ਰਹੇ ਸਨ, ਜਿਸਨੂੰ Realty Consultants ਮਈ 2026 ਦੀ ਰਿਪੋਰਟ ਢਾਂਚਾਗਤ ਤੌਰ 'ਤੇ (structurally) ਖੁੱਲ੍ਹੇ ਬਾਜ਼ਾਰ (open market) ਦੇ ਲੈਣ-ਦੇਣ (transacted) ਕੀਮਤਾਂ ਤੋਂ ਹੇਠਾਂ ਦੱਸਦੀ ਹੈ। ਉਸ ਖਰੀਦ ਨੂੰ ਮਜ਼ਬੂਤ ਵਾਧਾ (strong appreciation) ਪੈਦਾ ਕਰਨ ਵਾਲੀ ਚੀਜ਼ ਉਹਨਾਂ ਦਾ ਆਮਦਨ ਪੱਧਰ (income level) ਨਹੀਂ ਸੀ — ਇਹ ਸੀ ਕਿ ਉਹਨਾਂ ਨੇ ਜੋ ਉਤਪਾਦ (product) ਖਰੀਦਿਆ ਉਹ GMADA ਬੁਨਿਆਦੀ ਢਾਂਚਾ ਡਿਲੀਵਰੀ (GMADA infrastructure delivery), ਕਾਨੂੰਨੀ ਸਿਰਲੇਖ ਸਪੱਸ਼ਟਤਾ (legal title clarity), ਅਤੇ ਇੱਕ ਰੈਗੂਲੇਟਰੀ ਢਾਂਚੇ (regulatory framework) ਦੇ ਨਾਲ ਆਇਆ ਜੋ ਕਈ ਪ੍ਰਸ਼ਾਸਨਾਂ (administrations) ਵਿੱਚ ਕਾਇਮ (held) ਰਿਹਾ।

ਇੱਕ ਖਰੀਦਦਾਰ ਜਿਸਨੇ ਇੱਕ ਬਾਹਰੀ (peripheral) Kharar ਪ੍ਰਾਜੈਕਟ (project) ਵਿੱਚ ਘੱਟ ਕੀਮਤ ਬਿੰਦੂ (price point) 'ਤੇ ਖਰੀਦਿਆ ਸੀ, ਉਸਨੂੰ ਆਮਦਨ ਦੇ ਲਿਹਾਜ਼ ਨਾਲ ਜ਼ਰੂਰੀ ਤੌਰ 'ਤੇ ਬੁਰਾ ਸੌਦਾ (worse deal) ਨਹੀਂ ਮਿਲਿਆ। ਉਹਨਾਂ ਨੂੰ ਜੋ ਮਿਲਿਆ ਉਹ ਵਧੇਰੇ ਰੈਗੂਲੇਟਰੀ ਅਨਿਸ਼ਚਿਤਤਾ (regulatory uncertainty), ਬੁਨਿਆਦੀ ਢਾਂਚਾ ਜੋ ਡਿਵੈਲਪਰ ਦੀ ਡਿਲੀਵਰੀ ਸਮਰੱਥਾ (delivery capability) 'ਤੇ ਨਿਰਭਰ ਕਰਦਾ ਹੈ, ਅਤੇ ਕਾਨੂੰਨੀ ਨਿਵਾਰਣ (legal recourse) ਜੋ RERA ਤੋਂ ਪਹਿਲਾਂ ਕਮਜ਼ੋਰ (weaker) ਸੀ ਅਤੇ ਹੁਣ ਬਿਹਤਰ (better) ਹੈ।

ਜੋ ਅਭਿਸਰਣ (convergence) ਹੋ ਰਿਹਾ ਹੈ — RERA ਲਾਗੂਕਰਨ (enforcement) ਬਾਹਰੀ (peripheral) ਪ੍ਰਾਜੈਕਟਾਂ (projects) ਨੂੰ ਪਾਲਣਾ (compliance) ਵਿੱਚ ਲਿਆ ਰਿਹਾ ਹੈ, GMADA ਬੁਨਿਆਦੀ ਢਾਂਚਾ ਠੇਕੇ (infrastructure contracting) Banur ਅਤੇ Kharar ਪੱਟੀਆਂ (belts) ਵੱਲ ਵਧ ਰਿਹਾ ਹੈ, Kharar-Landran STP ਜੁਲਾਈ ਵਿੱਚ ਚਾਲੂ (commission) ਹੋਣ ਦੀ ਉਮੀਦ ਹੈ — ਇਹ ਉਹ ਵਿਧੀ (mechanism) ਹੈ ਜਿਸ ਰਾਹੀਂ ਕੀਮਤ ਦਾ ਕੁਝ ਪਾੜਾ (price gap) ਅੰਤ ਵਿੱਚ ਬੰਦ (closes) ਹੁੰਦਾ ਹੈ। ਇਹ ਜਲਦੀ ਬੰਦ ਨਹੀਂ ਹੁੰਦਾ, ਅਤੇ ਇਹ ਇਕਸਾਰ (uniformly) ਬੰਦ ਨਹੀਂ ਹੁੰਦਾ। ਪਰ ਇਹ ਬੰਦ ਹੁੰਦਾ ਹੈ, ਜਿਵੇਂ ਕਿ ਸੈਕਟਰ 108, 109, ਅਤੇ 114 ਵਿੱਚ ਬਾਹਰੀ ਚਾਪ (outer arc) ਵਾਧੇ (appreciation) ਦੀ ਕਹਾਣੀ ਪ੍ਰਦਰਸ਼ਿਤ (demonstrates) ਕਰਦੀ ਹੈ।

ਤਿੰਨ ਸਾਲ ਪਹਿਲਾਂ ਉਹ ਸੈਕਟਰ (sectors) ਬਾਹਰੀ (peripheral) ਬਾਜ਼ਾਰ ਸਨ। ਉਹ ਹੁਣ ਨਹੀਂ ਹਨ।

---

ਸਰੋਤ (Sources)

- 99acres — ਜਾਇਦਾਦ ਦੀਆਂ ਦਰਾਂ ਅਤੇ ਕੀਮਤ ਰੁਝਾਨ (Property rates and price trends), Aerocity Mohali, Kharar, Banur, Sector 92, ਜੂਨ 2026

- 99acres — ਸਭ ਤੋਂ ਵੱਧ ਸਰਾਹੇ ਗਏ ਇਲਾਕੇ (Most appreciated localities) Mohali, ਫਰਵਰੀ 2026 (Sector 108: 112.4%, Sector 109: 107.5% ਤਿੰਨ ਸਾਲਾਂ ਵਿੱਚ)

- Realty Holding and Management Consultants — ਜਾਇਦਾਦ ਦੀਆਂ ਦਰਾਂ Mohali 2026 ਜ਼ਮੀਨੀ-ਪੱਧਰ ਦੀ ਰਿਪੋਰਟ (ground-level report), 14 ਮਈ, 2026

- GMADA ਮਾਰਚ 2026 ਨੀਲਾਮੀ ਦੇ ਨਤੀਜੇ (auction results) — Rs 3,137 ਕਰੋੜ, ਰਿਜ਼ਰਵ (reserve) ਤੋਂ 55% ਪ੍ਰੀਮੀਅਮ (premium), Aerocity ਹਾਊਸਿੰਗ ਸਾਈਟ Rs 311.74 ਕਰੋੜ

- Mohali Aerotropolis — RERA ਲਾਗੂਕਰਨ ਕਵਰੇਜ (enforcement coverage) ਅਤੇ PPCB ਸੀਵਰੇਜ ਕੇਸ (sewage cases), ਜੂਨ 2026